Data & Analysis

Every scan, reasoning trace, and price follow-up produced by this agent is viewable on this site. The underlying dataset is shared for non-commercial research only; bulk export is gated behind an access password — contact the authors to request access. This page also links to the chart set we use in our ICML workshop paper. Charts are regenerated from the live database, so they will shift as more scans accumulate.

Pull the data

The full source code, including the pipeline, analysis scripts, and figure generators, lives on GitHub:

github.com/wyw2010/forecasting-agent →

All data endpoints return JSON. The primary endpoint is a single-shot dump of every scan, trace, trade, price follow-up, and P&L snapshot:

curl -H "Authorization: Bearer ACCESS_PASSWORD" https://forecast.agenticlearning.ai/api/export > export.jsonOr export straight from the browser — enter the access password and download the full JSON dump:

| Endpoint | What it returns |

|---|---|

/api/export |

Full JSON dump: scans, V2 reasoning traces, trades, price follow-ups, P&L snapshots, summary.

Archived scans are excluded by default; pass

?include_archived=true to include them.

🔒 Access password required.

|

/api/metaculus/export |

Full JSON dump of the Metaculus tournament-bot traces (separate from the Kalshi

scanner data above): each question's submitted forecast plus the full reasoning trace.

Use post_id / question_id to look up resolutions via the Metaculus API.

Pass ?include_trace=false for a metadata-only dump.

🔒 Access password required.

|

/api/scans |

Most recent 200 scans with market, prediction, edge, and confidence. 🔒 Access password required. |

/api/trades |

Paper-trade log. Optional ?status=open|closed|all. 🔒 Access password required. |

/api/pnl |

Current P&L summary (totals, win rate, deployed capital). |

/api/pnl-series |

Full P&L time series with per-minute timestamps. |

/api/followups |

Price follow-ups at t+1…t+30 days for every scan. 🔒 Access password required. |

/api/trade/{id}/market-data |

Historical price series for one trade's market. |

To reproduce the analysis in the paper:

git clone https://github.com/wyw2010/forecasting-agent && cd forecasting-agentcurl -H "Authorization: Bearer ACCESS_PASSWORD" https://forecast.agenticlearning.ai/api/export > data/export_latest.jsonpulls the latest export (request the access password from the authors).python analysis/extract_factors.py --input data/export_latest.json --output analysis/output/factors.csvextracts per-scan factors from the reasoning traces.python analysis/compute_directional_accuracy.py --factors analysis/output/factors.csv --data data/export_latest.json --output analysis/output/factors_with_da.csvjoins the factors with price follow-ups.python analysis/generate_figures.py --out-dir out/ --min-date 2026-04-07 --data data/export_latest.jsonproduces the headline charts below.python analysis/generate_ablation_figures.py --out-dir out/ --min-date 2026-04-07 --horizon 3produces the pipeline and tool ablations.

Headline charts

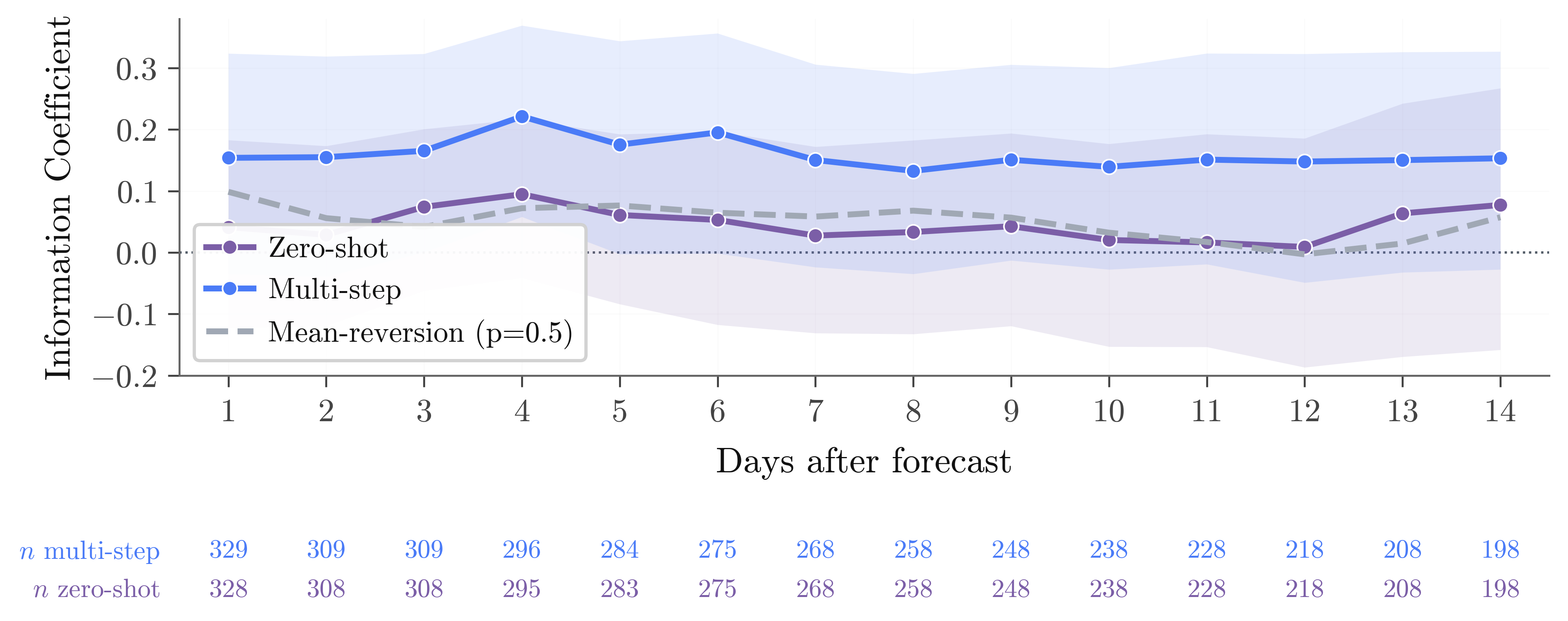

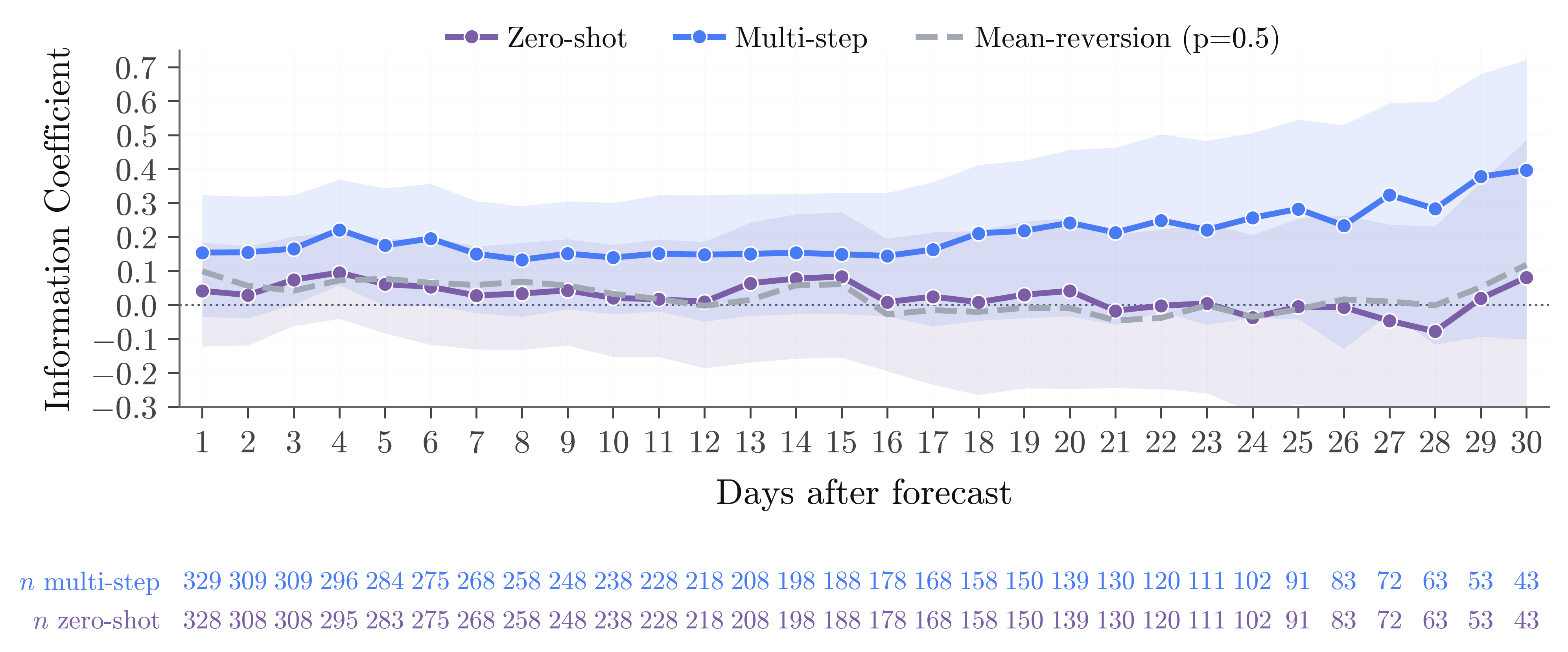

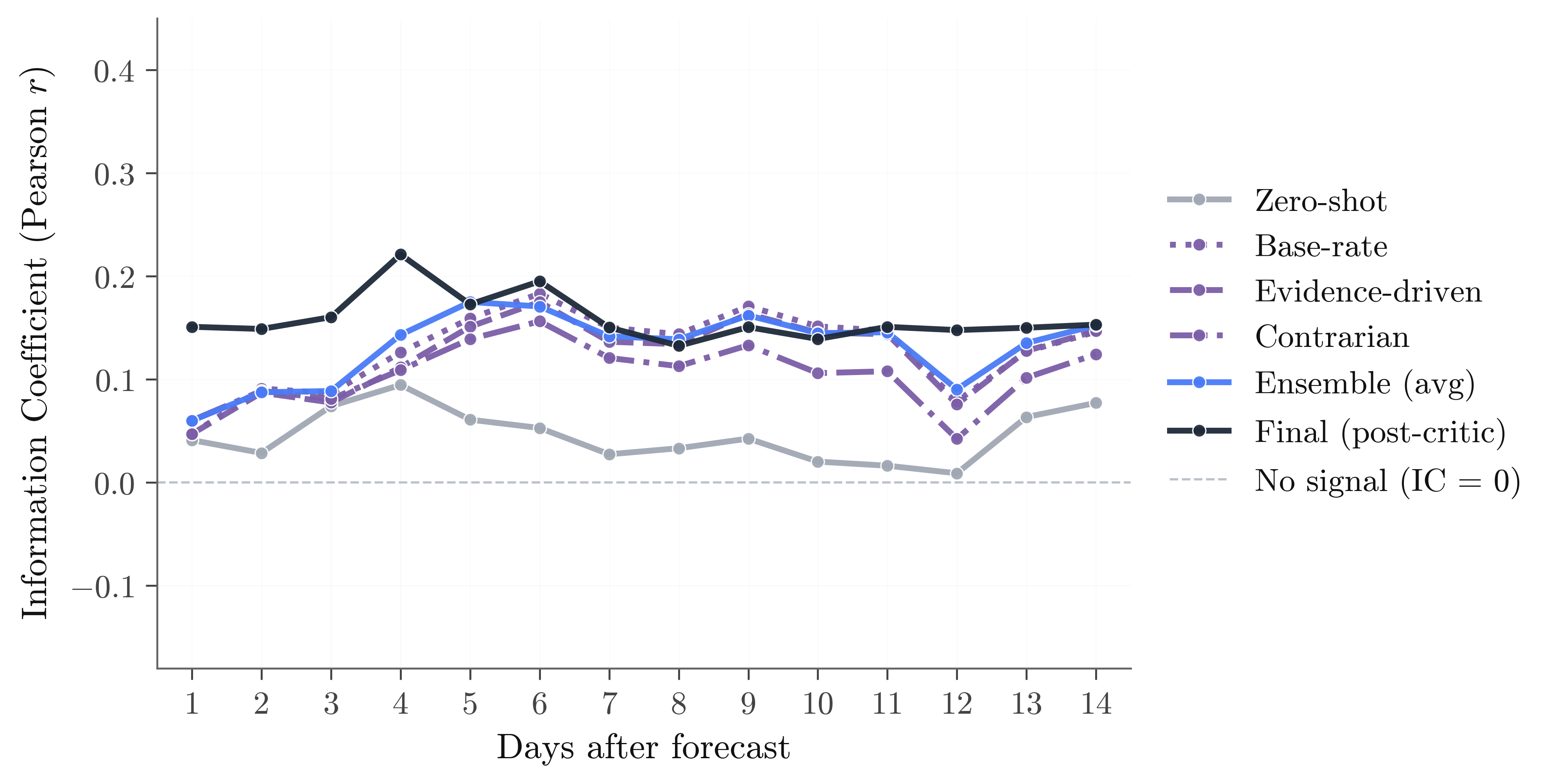

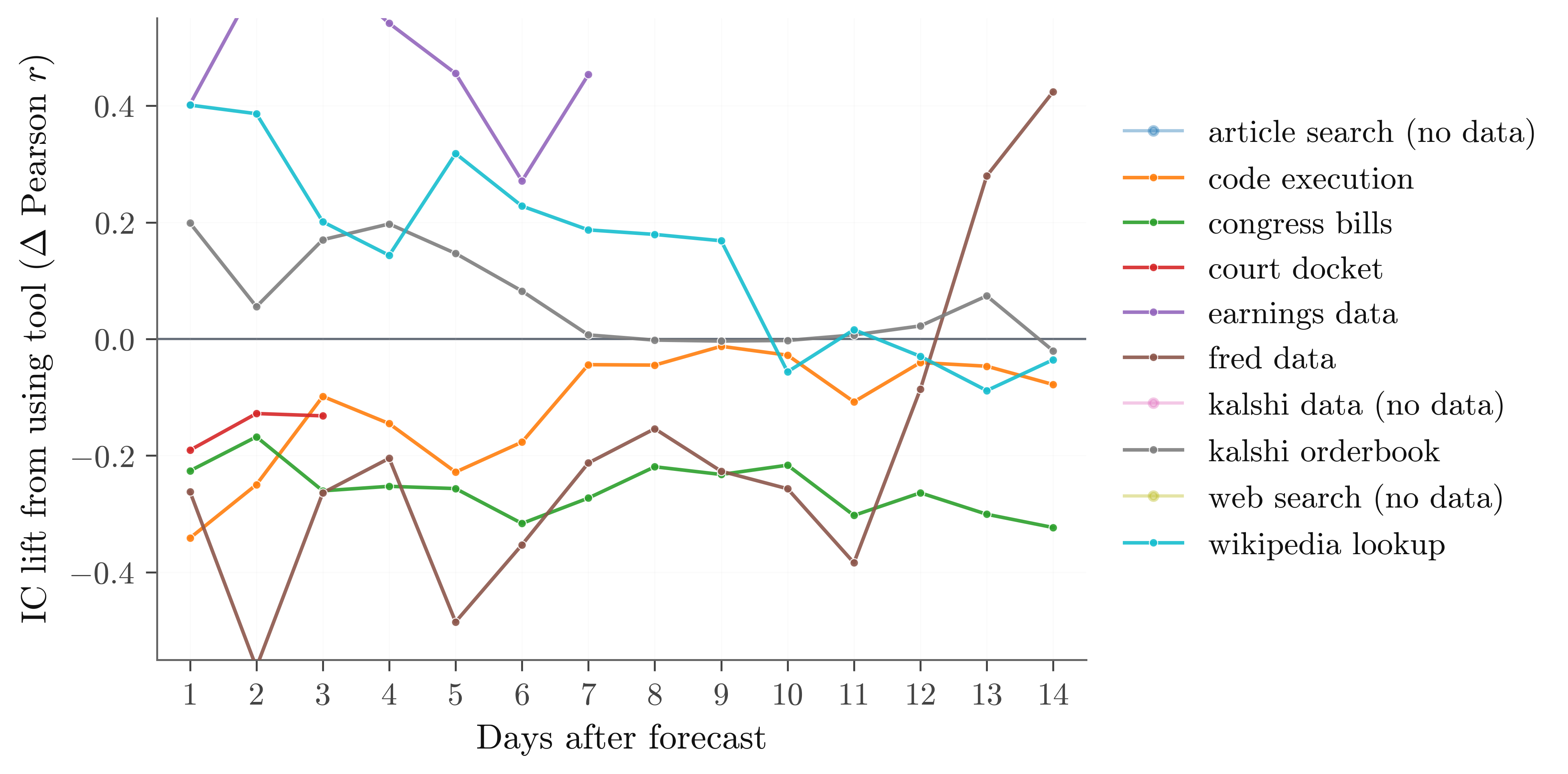

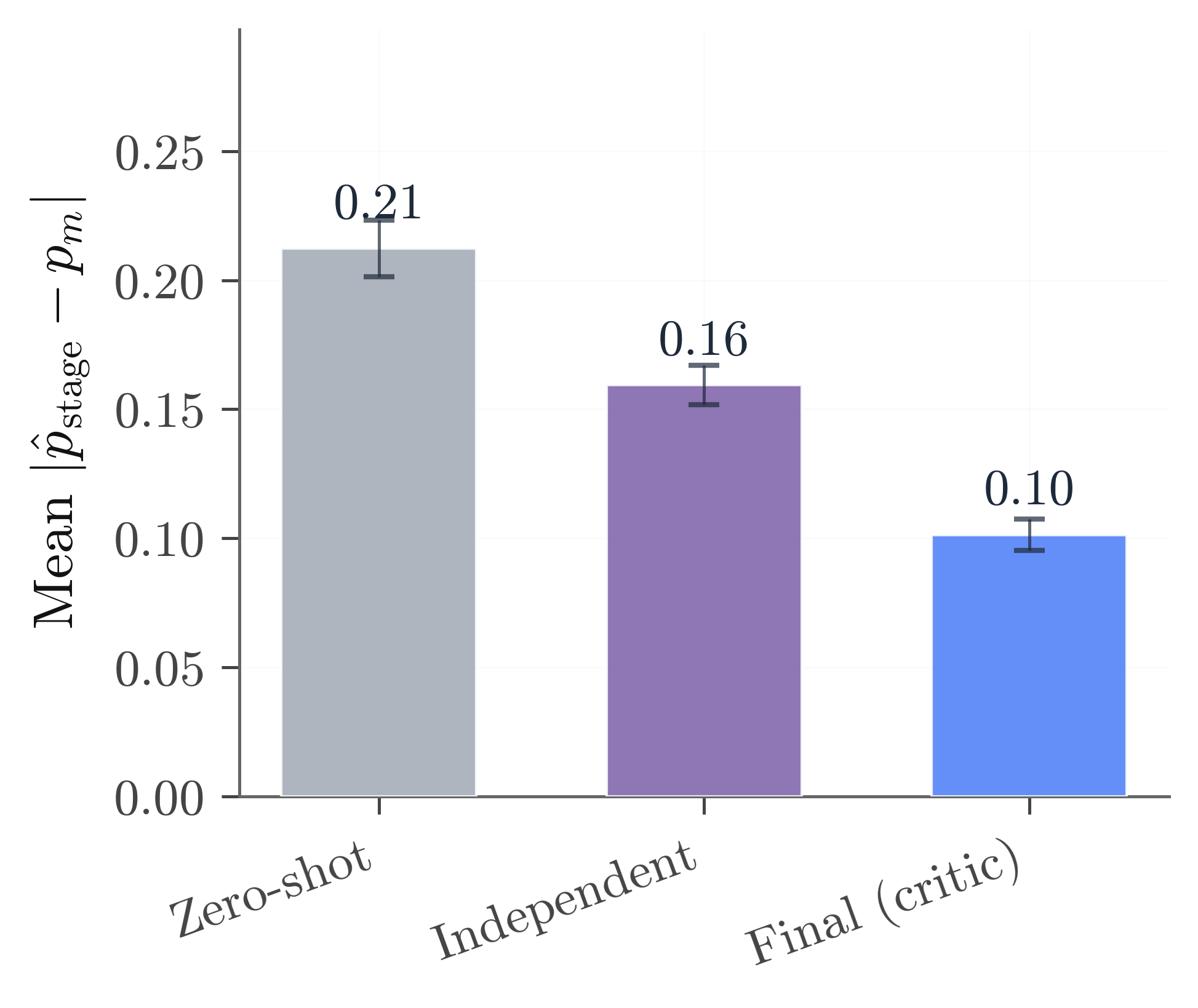

Four charts carry the paper's main story. They answer, in order: does our agent beat a simple baseline? · which stage of the pipeline did the work? · which research tool did the work? · does the critic stage actually help, or just hug the market?

Multi-step averages IC +0.17 across t+1 through t+14 vs. +0.02 for zero-shot and +0.04 for mean-reversion. The multi-step pipeline beats both baselines at every horizon, and the gap widens at longer horizons.

Supporting evidence

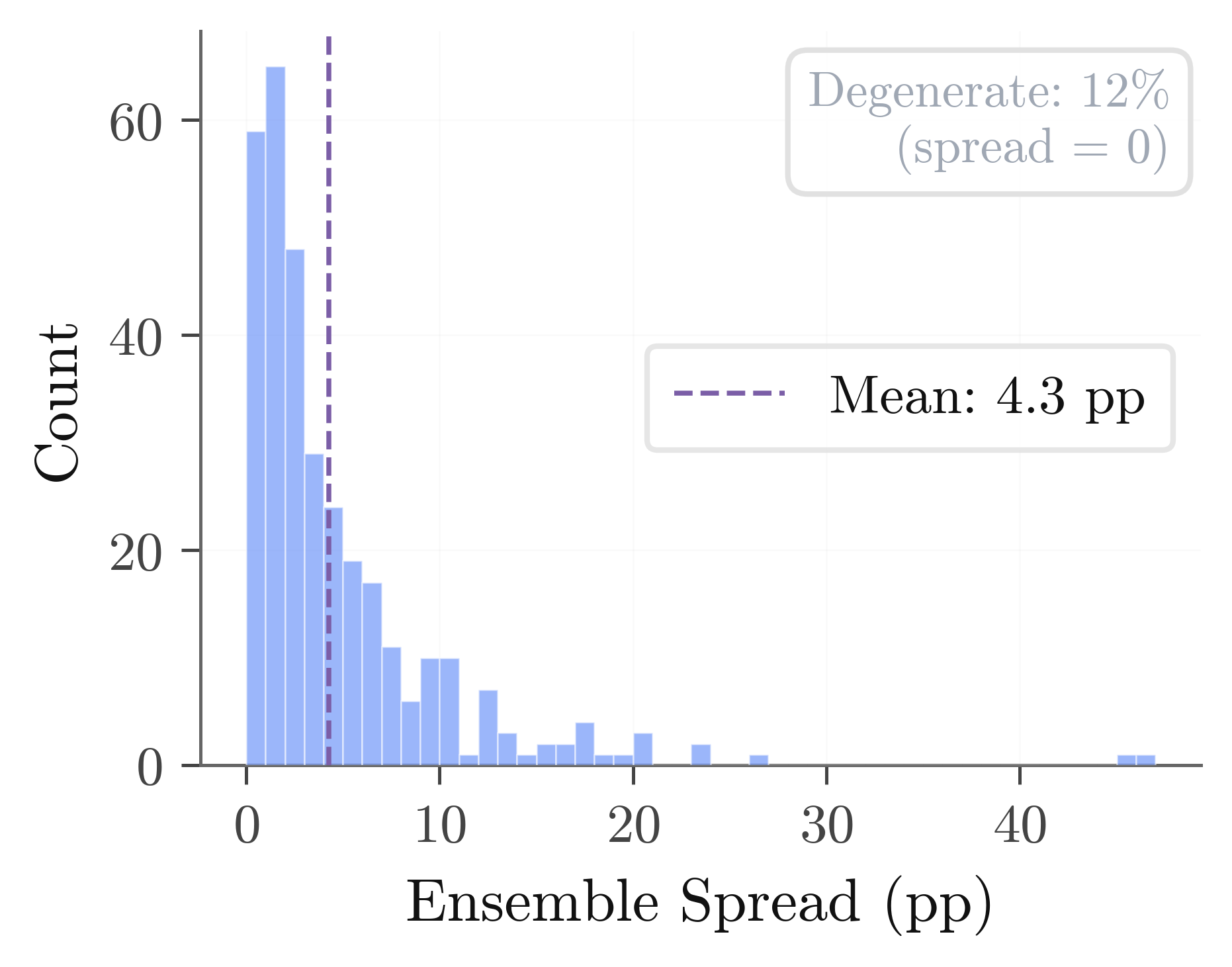

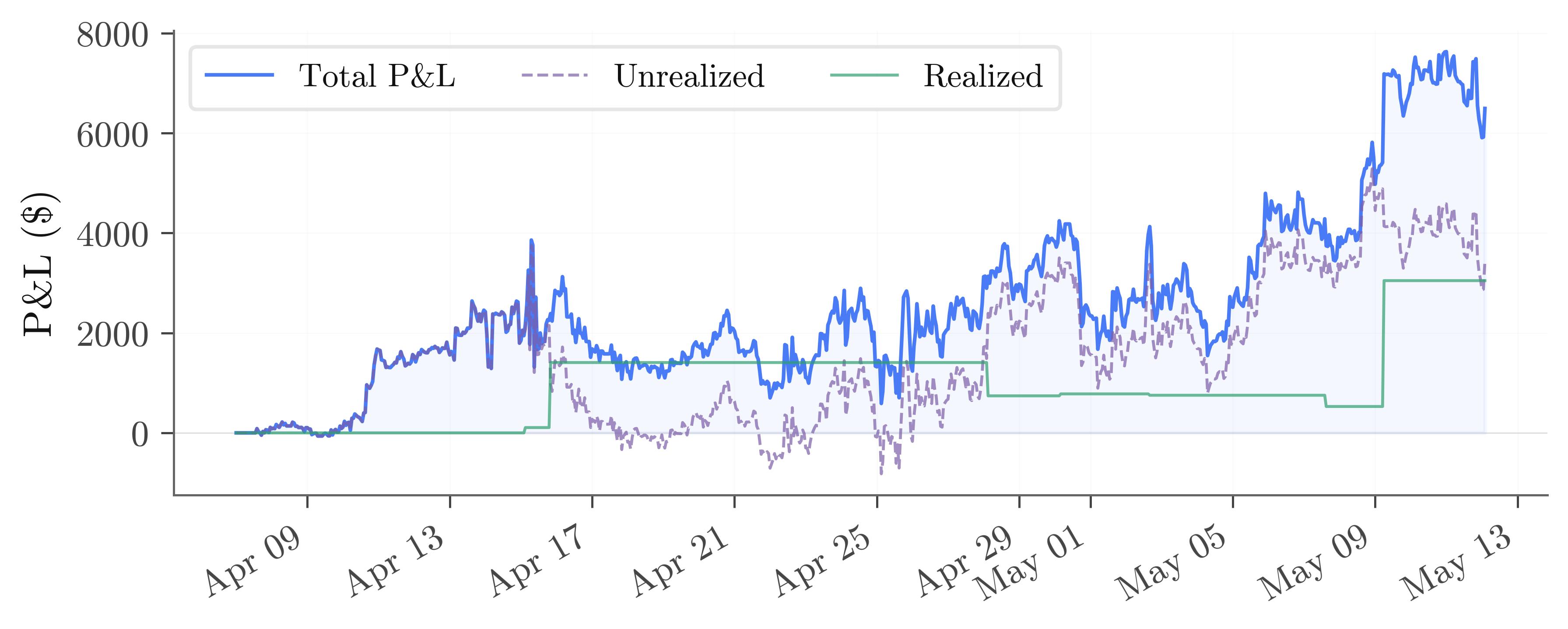

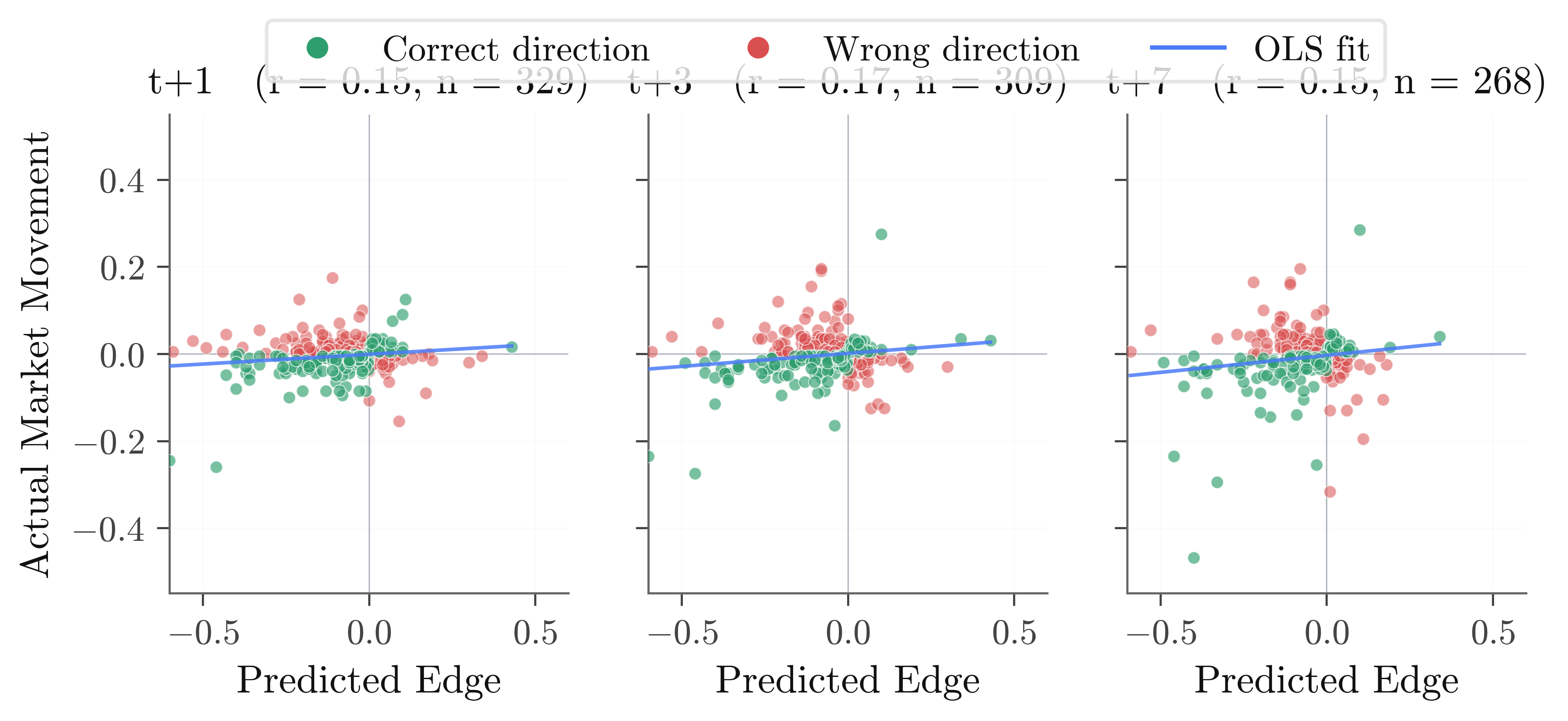

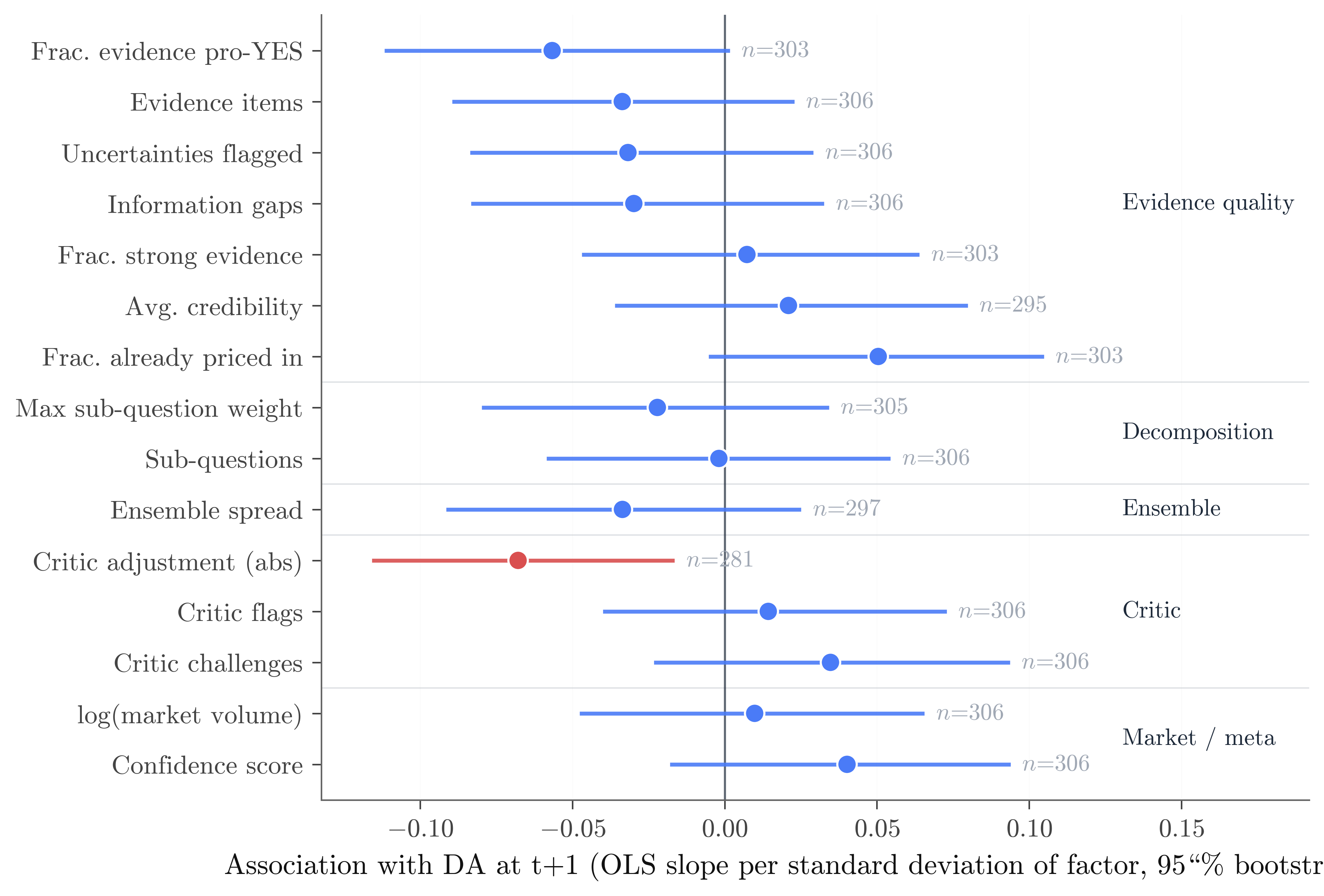

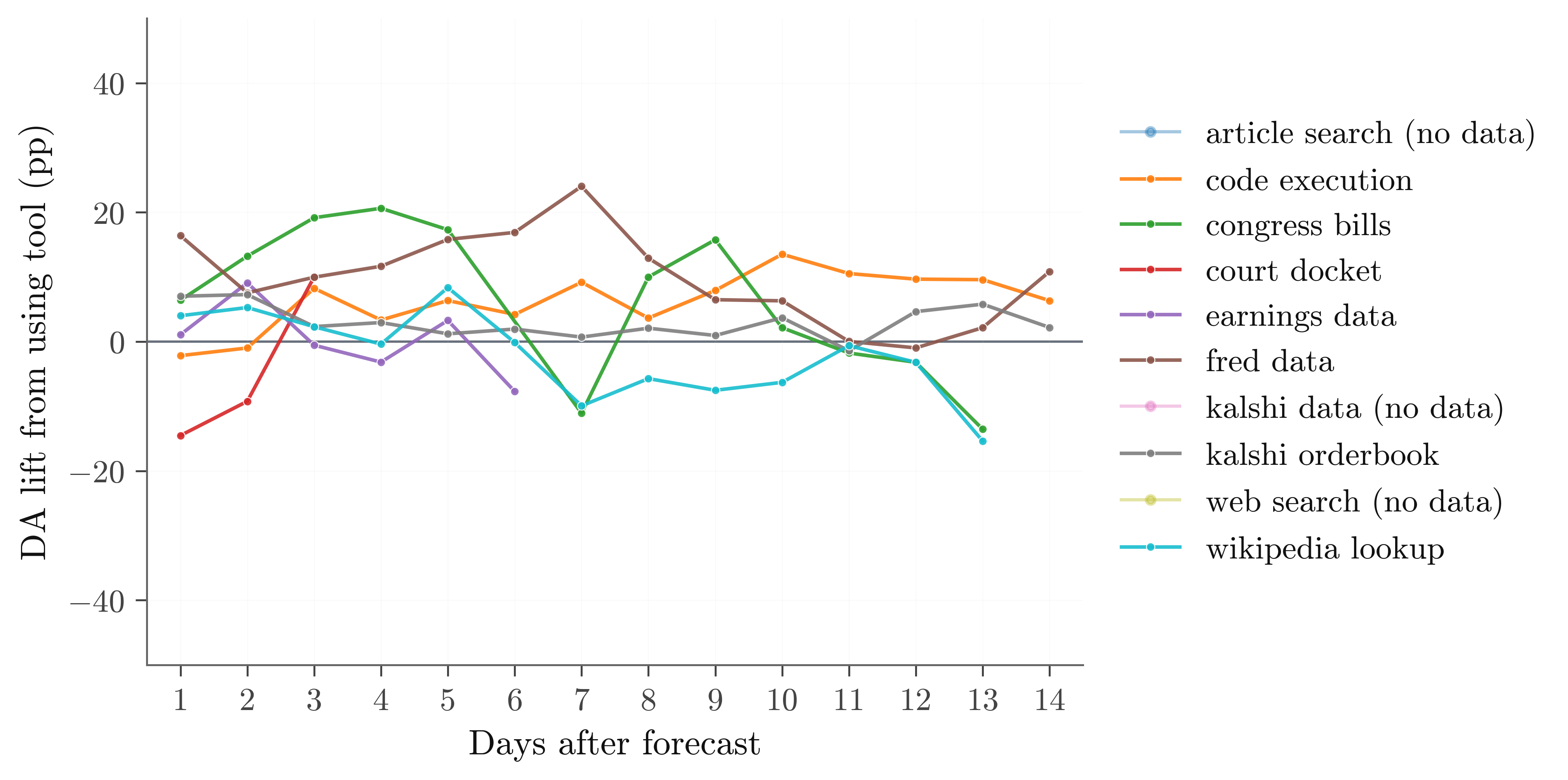

Diagnostic panels that back up the headline story: the ensemble's diversity collapse, the cumulative paper-trading P&L (an economic-value sanity check on the IC lift), the relationship between forecast magnitude and subsequent movement, and a regression forest plot of every non-tool factor.

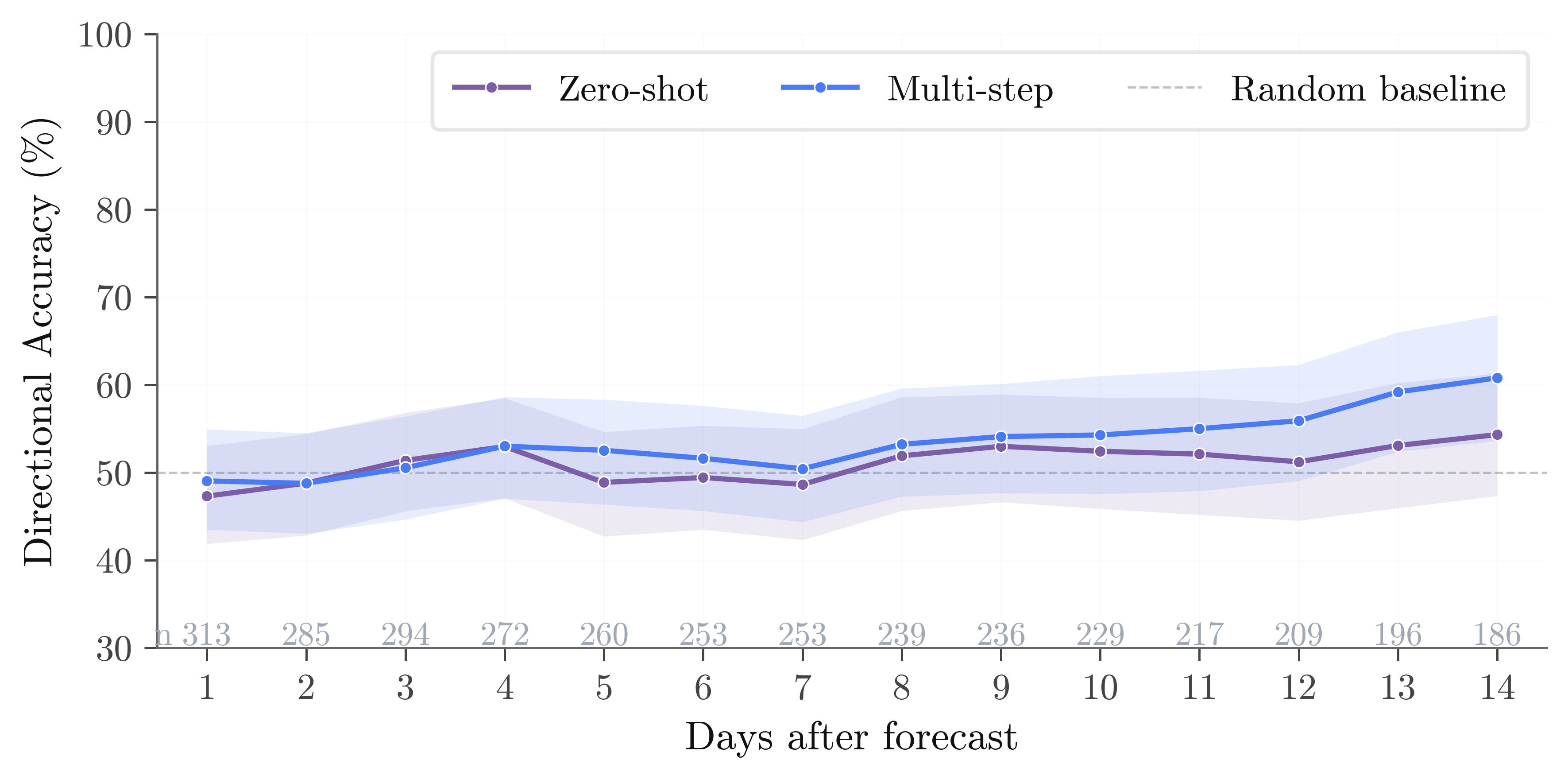

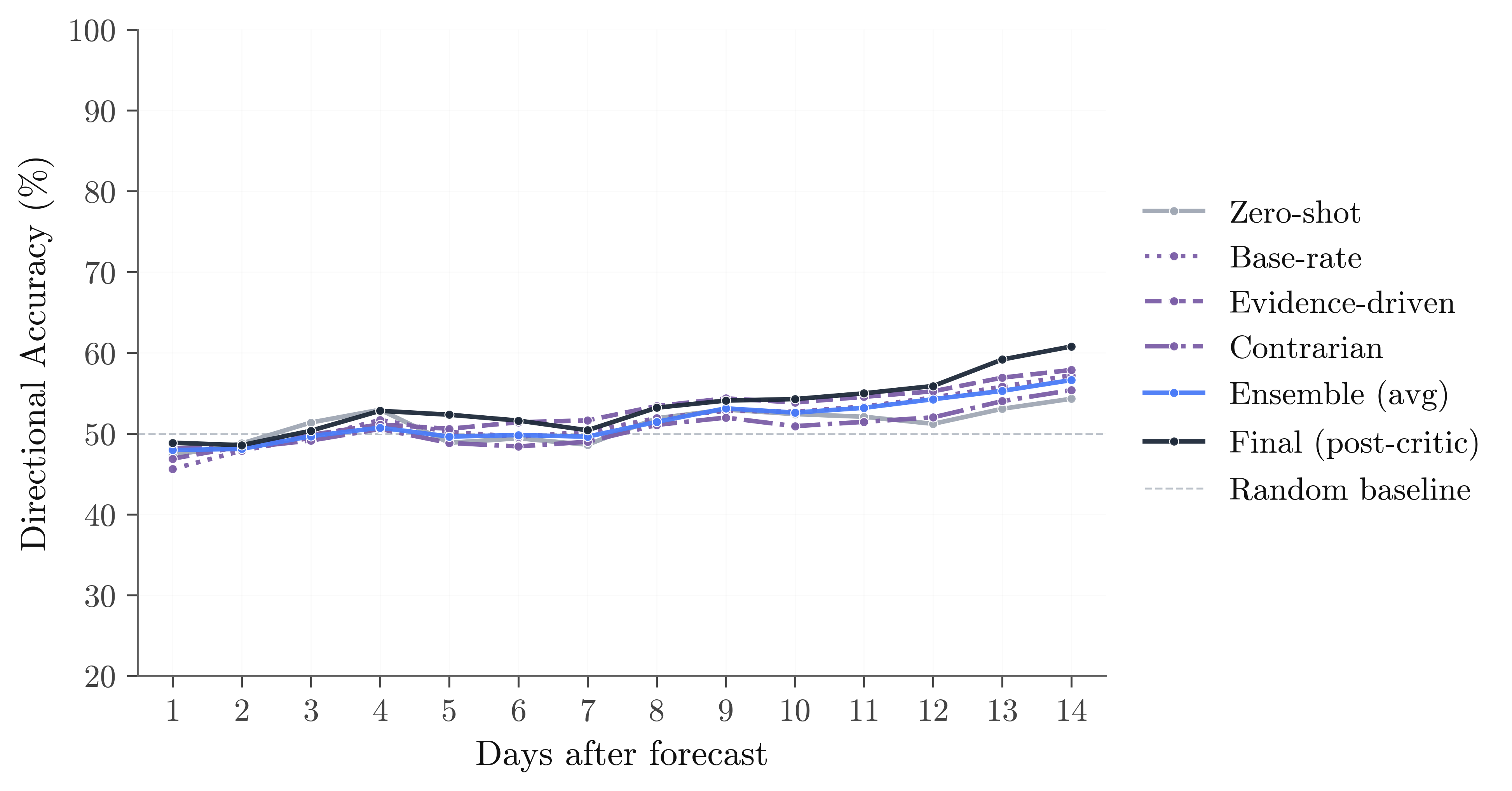

Directional accuracy companions

Directional accuracy (DA) asks the simpler binary question: did the market move in the direction we predicted? The IC findings hold qualitatively under DA, but with markedly smaller effect sizes, consistent with DA discarding the magnitude information IC retains. We keep DA charts here for comparison with prior prediction-market work; IC is the primary headline.

Charts were last regenerated from the figures_apr7plus cohort (259 V2 scans,

archived excluded). The analysis scripts and chart templates are in analysis/

on GitHub;

rerun them against a fresh /api/export pull to reproduce.